If you are an expert or internet marketer selling high value courses in the UK (such as a Mastermind Group or a high level training/coaching course), you may (like it has become popular to do) offer payments in instalments to make it easier for your prospects to finance their purchase.

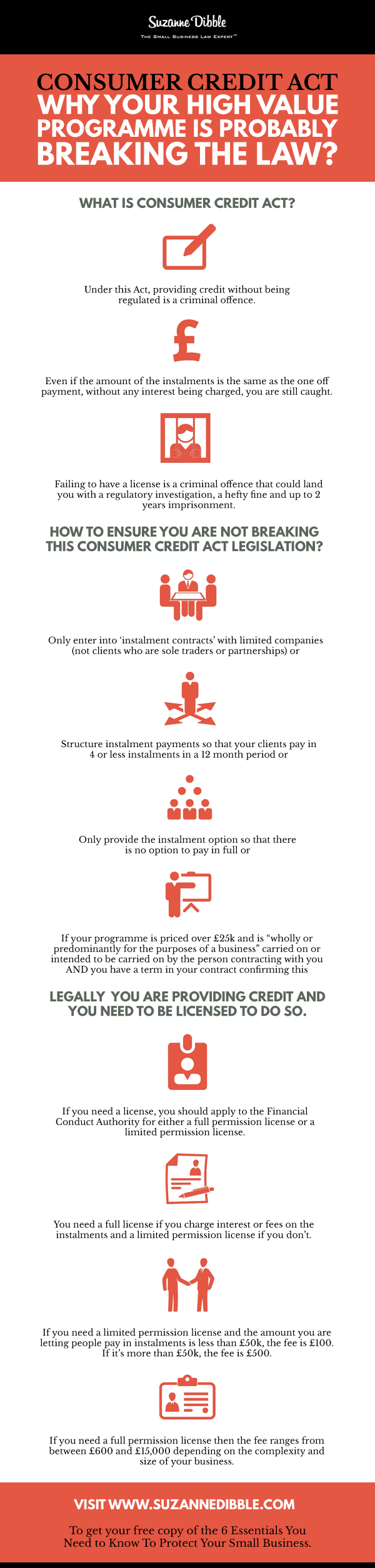

However you may unwittingly be in breach of the Consumer Credit Act. Under this Act, providing credit without being regulated is a criminal offence.

You may be caught by this “consumer” legislation even if you are selling to ‘businesses’, as sole traders and partnerships are also caught under the legislation.

Even if the amount of the instalments is the same as the one off payment, without any interest being charged, you are still caught.

Failing to have a license is a criminal offence that could land you with a regulatory investigation, a hefty fine and up to 2 years imprisonment.

Chances are that you would have to be doing something fairly calculating to be landed with a prison sentence – sheer ignorance of the law is more likely to be met with a fine, but don’t quote me on that as all the regulator will say is that cases are judged on a case by case basis.

In addition, any relevant agreement you had would not be enforceable meaning that if your clients didn’t pay up, you couldn’t pursue them.

So what can you do to ensure that you do not fall within this Consumer Credit Act legislation?

- only enter into ‘instalment contracts’ with limited companies (not clients who are sole traders or partnerships)

OR

- structure instalment payments so that your clients pay in 4 or less instalments in a 12 month period

OR

- only provide the instalment option so that there is no option to pay in full

OR

4. if your programme is priced over £25k and is “wholly or predominantly for the purposes of a business” carried on or intended to be carried on by the person contracting with you AND you have a term in your contract confirming this

Otherwise, legally you are providing credit (even if the amount of the instalments is the same as the one off payment, without any interest) and you need to be licensed to do so.

If you need a license, you should apply to the Financial Conduct Authority for either a full permission license or a limited permission license.

You need a full license if you charge interest or fees on the instalments and a limited permission license if you don’t.

If you need a limited permission license and the amount you are letting people pay in instalments is less than £50k, the fee is £100. If it’s more than £50k, the fee is £500.

If you need a full permission license then the fee ranges from between £600 and £15,000 depending on the complexity and size of your business.

To read more about applying for licenses go to //www.fca.org.uk/firms/firm-types/consumer-credit

UPDATE

As of 18 March 2015, the instalment exemption has been extended so that you can take up to 12 instalments in any 12 month period. However this extended exemption will not be available if the agreement to accept payment by instalments is entered into after the debt has been incurred (ie after the contract was formed). See more at //www.fca.org.uk/firms/firm-types/consumer-credit/instalment-exemption

This is the type of incredibly useful, practical information I share with my subscribers – to receive my special updates and free legal documents, just enter your email address below:

Contact Form

If you’re interested to know more and to ask your own questions to top business lawyer Suzanne Dibble and learn from the experience of lots of other small business owners, then click here to join our thriving membership!

© Suzanne Dibble 2013-2024

The information contained above is provided for information purposes only. The contents of this article are not intended to amount to advice and you should not rely on any of the contents of this article. Professional advice should be obtained before taking or refraining from taking any action as a result of the contents of this article. We disclaim all liability and responsibility arising from any reliance placed on any of the contents of this article.